It’s been a strange few months in economic news, and two reports this week from the Bureau of Labor Statistics (second-quarter Productivity and Costs and the July Consumer Price Index) continue that trend—but we’re heading in the right direction.

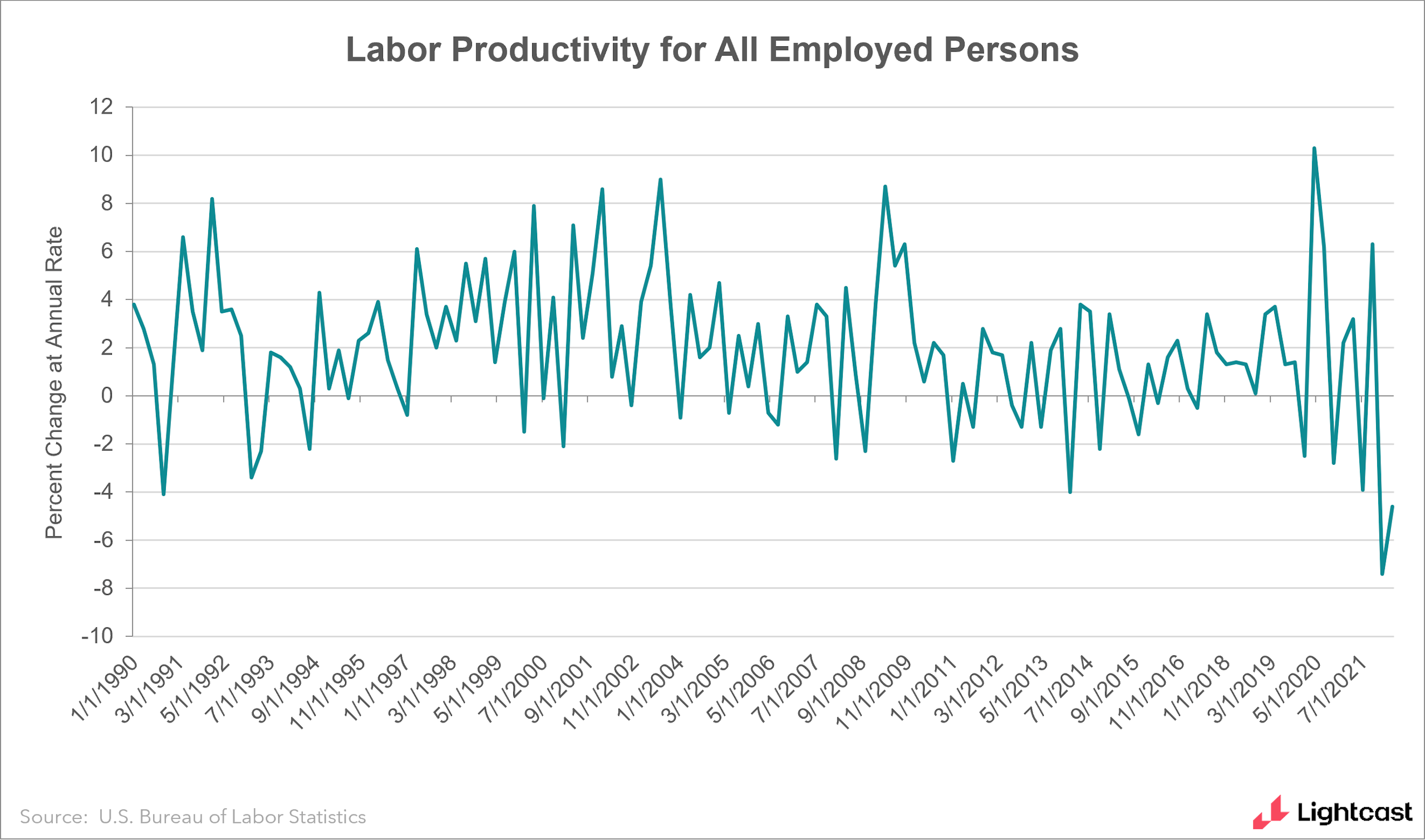

The CPI made more headlines, but I’ll start with Productivity and Costs, which is no less important for understanding the current economic situation. The BLS reports that productivity (in the nonfarm business sector) fell 4.6% in the second quarter of 2022, and first-quarter productivity was revised down slightly to 7.4%. That’s the largest year-over-year rate drop since the BLS started tracking productivity in 1948.

At first, that obviously looks like very bad news. But not so fast: I think it’s only kind-of-bad news.

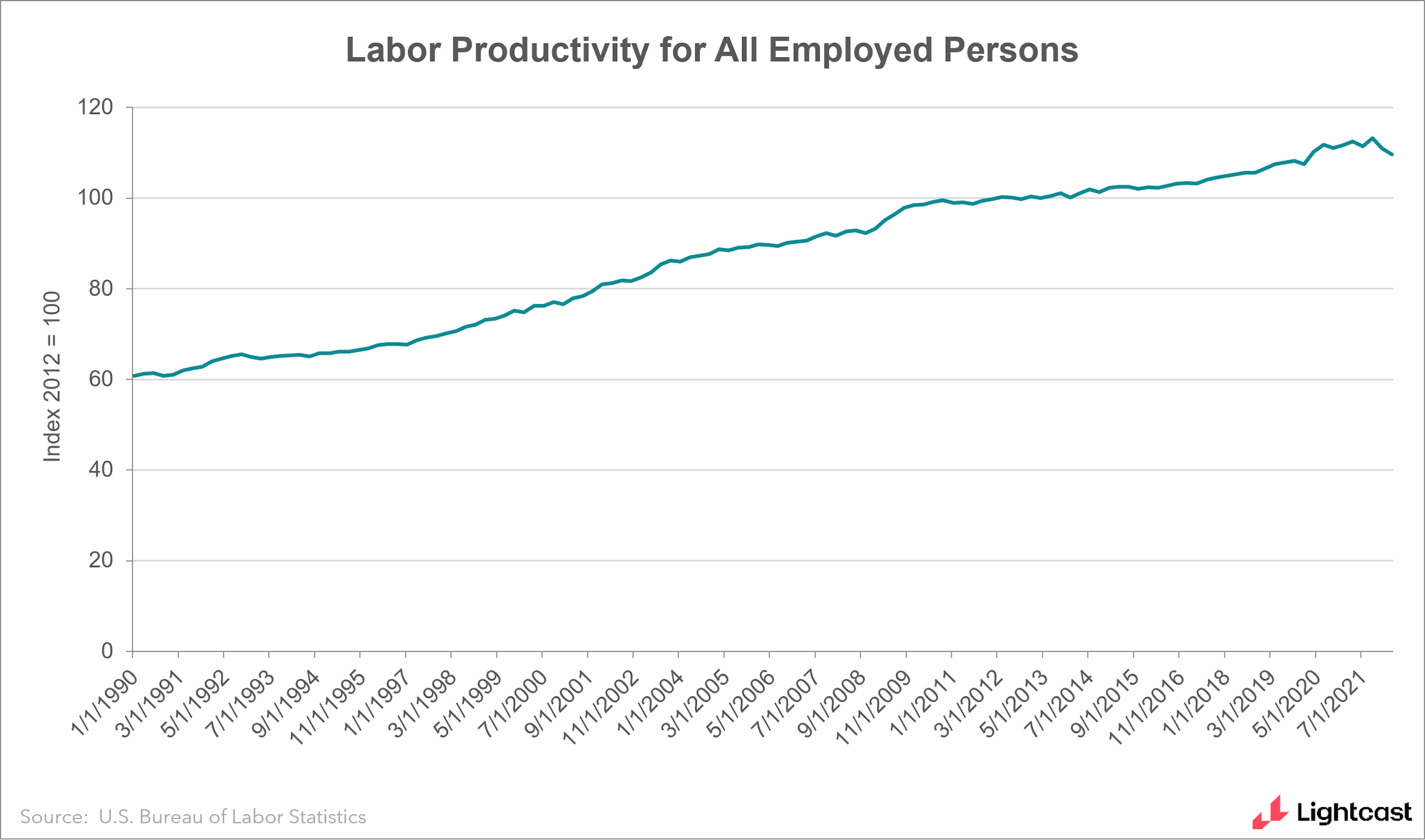

This graph and media reports focus on how productivity changes quarter-by-quarter, not the overall indexed level of change, and that means they don’t reflect the overall pattern of how productivity has changed over time. That measure shows much more stability than the jagged line above.

Taking this view, productivity has been increasing steadily overall since 1948, even improving since the pandemic. But here’s the catch: since Q4 of 2019, labor productivity has increased 1.4% total, or 0.6% annually—well below its 2% historic average.

So why have the last two years been less productive than their historical levels? Here are four ideas.

High churn and high quits. If you have to keep hiring new people, it takes time to get them up to speed. In a normal labor market, high turnover after a recession is related to higher productivity. But this time is different: churn is so high that its main result has been disruption, instead of workers finding better fits.

Covid-19 changed company practices. When companies changed how they operated during the pandemic, whether by adding new cleaning practices or other moves away from business as usual, productivity fell.

The impact of working from home is up for debate. While much of the data I’ve seen supports the idea that hybrid or remote work increases productivity, it’s still an open question, and not everyone agrees—more on this in a moment.

Businesses are hoarding their workers. The June JOLTS showed that layoffs are still near a record low, even declining slightly since May. Hardly any employers are getting rid of their existing workforce, likely because the tight labor market has led to fears they wouldn’t be able to get workers back if they need them. This could be keeping businesses from using their workers in the most efficient and productive way possible.

Whatever the reason for decreased productivity, our economy is not doing as badly as the headline numbers suggest—this isn’t the worst things have been since 1948. However, the Productivity and Costs report does show that there are misallocations and inefficiencies still lingering, suggesting we have room to grow.

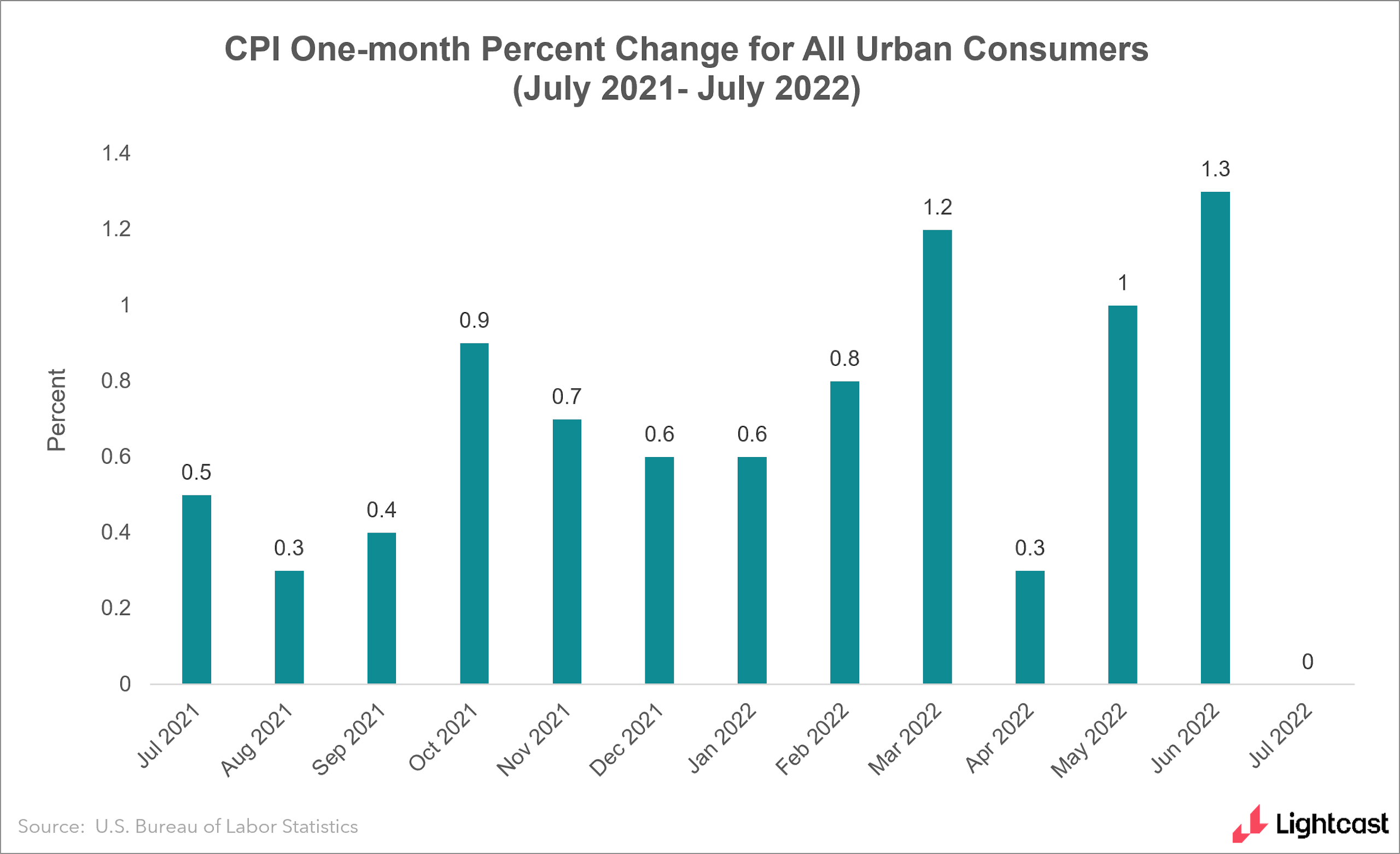

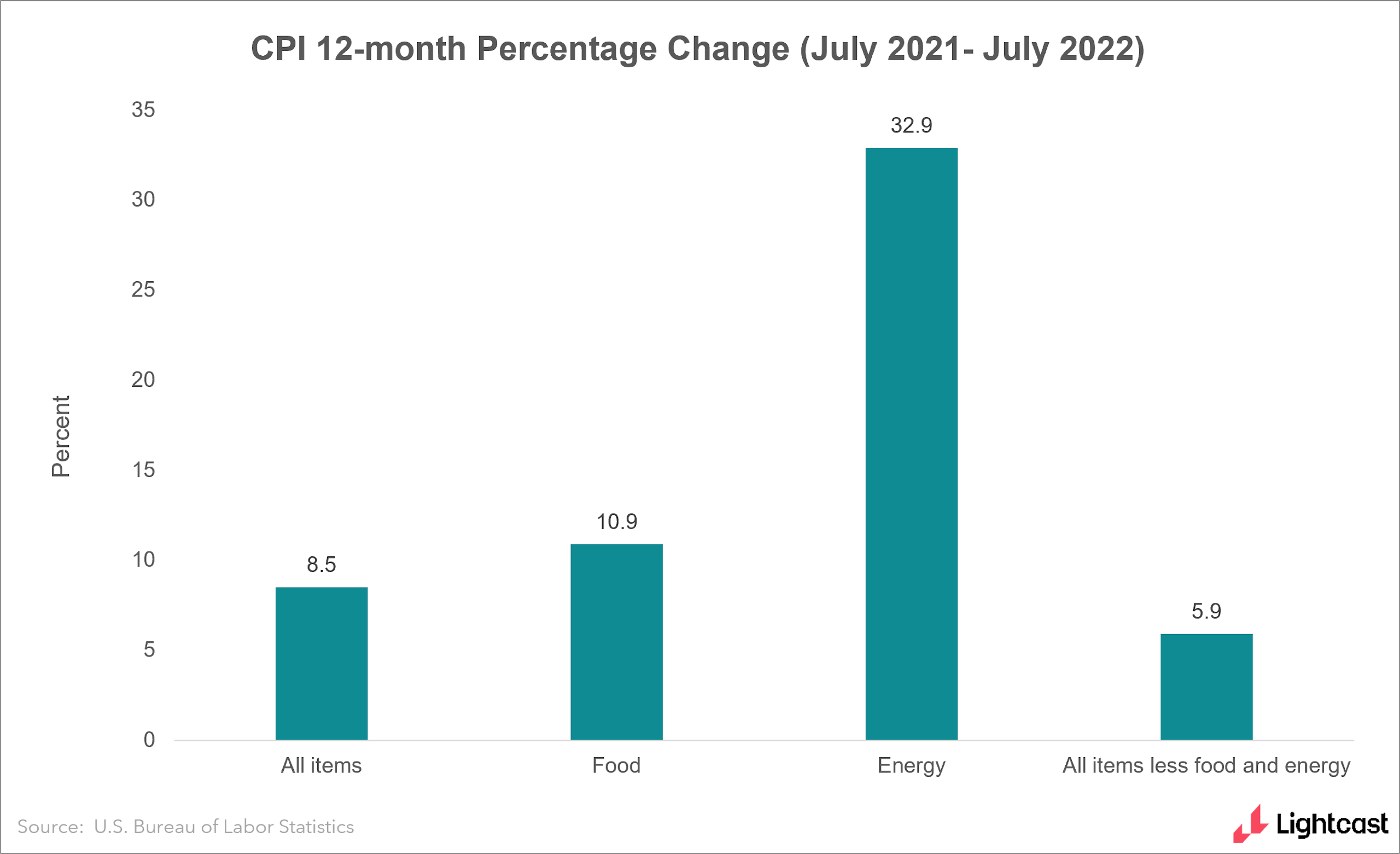

Now onto the CPI, which showed that inflation in July dropped to zero!

The report also showed that core CPI (excluding food and energy) rose 0.3%, below expectations of 0.5% and significantly lower than its 0.7% rise in June. But just like with productivity, looking just at one aspect of this data keeps us from looking at the big picture. Over the past twelve months, prices have risen 8.5%, which is far from ideal.

In fact, the best way to understand what the data tell us about the economy and labor market is to take these two reports together, looking a little deeper in the weeds.

Unit labor costs in the nonfarm business sector increased 10.8% in the second quarter of 2022, reflecting a 5.7% increase in hourly compensation but a 4.6% decrease in productivity. Over the last four quarters, labor costs increased 9.5%—the largest four-quarter increase since Q1 1982!

What does all that mean? It implies that if prices can stay under control, the cost of labor will be one of the main factors affecting price increases. So while the ongoing worker shortage is great for those looking for a job, the impact might be felt in prices going up for everyone.

In The Papers

Like I mentioned, the data I’ve seen so far points in favor of working from home, or at least a hybrid arrangement. “How Hybrid Working From Home Works Out,” by Nicholas Bloom, Ruobing Han, and James Liang, contributes some compelling evidence for that case. In the hybrid situations the authors studied:

Attrition dropped by 35% and employees reported higher work satisfaction scores, highlighting that workers place considerable value on this amenity

The nature of the workweek changed, with fewer hours being worked during “home” days but more in the evening or weekend.

Hybrid employees sent more messages and made more video calls, even when in the office, showing the rise of new modes of communication.

Working from home had a small positive impact on productivity.

Overall, these results show that working from home, at least in the settings studied, had benefits for both employees and employers. And during a complex time in the labor market, those benefits go a long way.

Until next week,

Bledi Taska

Lightcast Chief Economist