Happy New Year, and welcome (back) to the Letter from the Chief Economist!

With three big economic news releases out less than two weeks into 2023, we’ve started the year off with a bang. Let’s run through them in order.

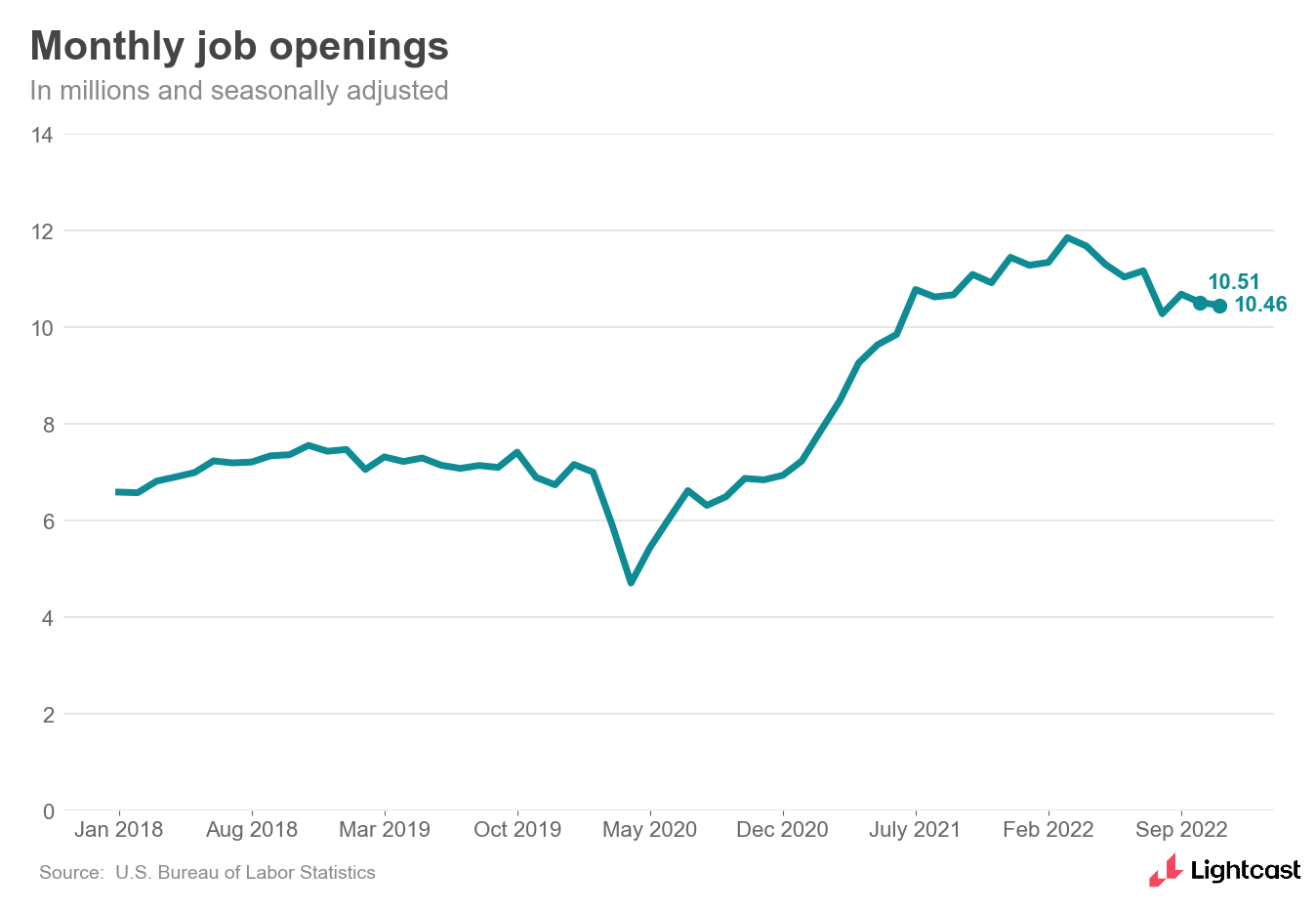

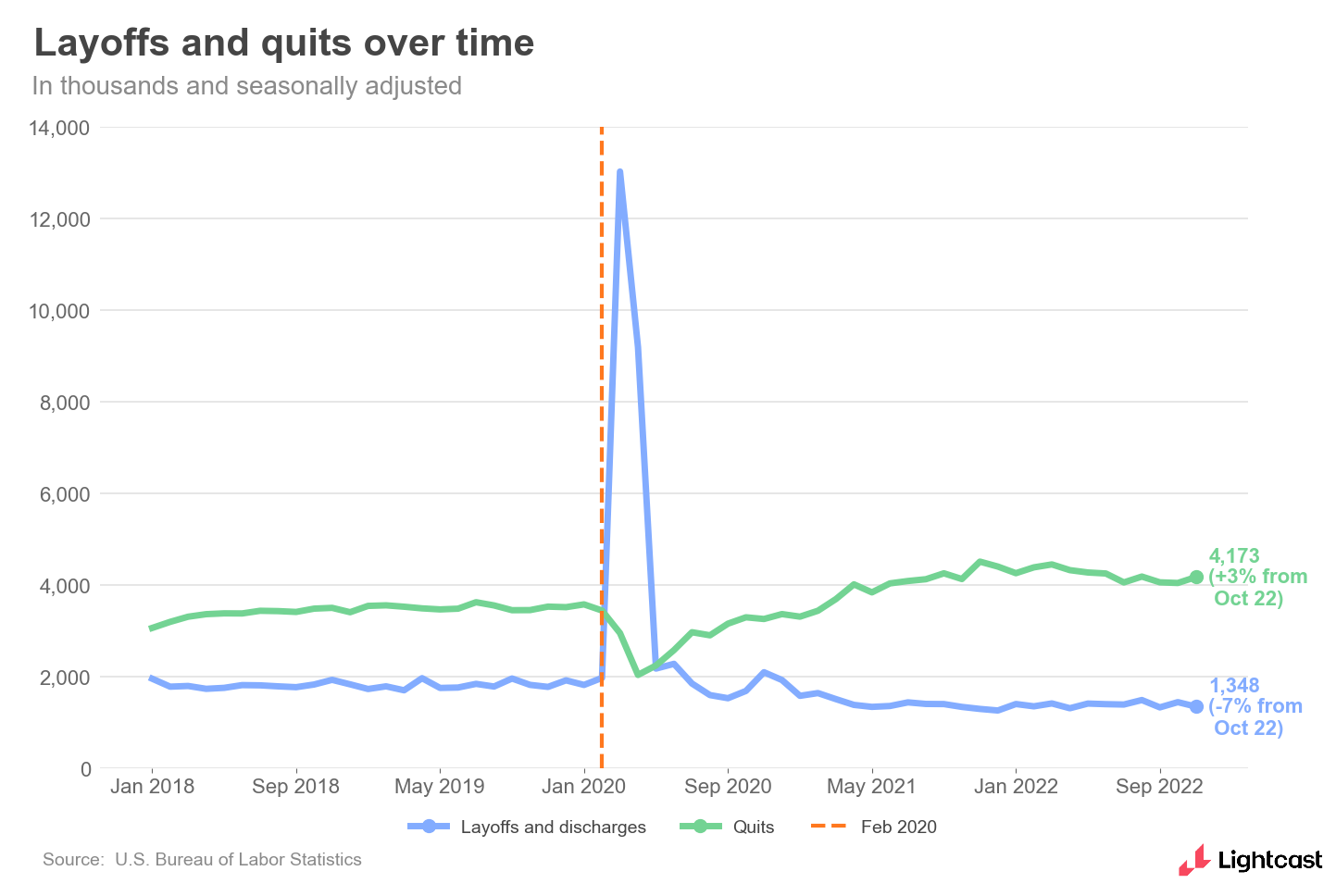

Last Wednesday, JOLTS (the Job Openings and Labor Turnover Survey) came in stronger than expected. Overall openings were little changed at 10.5 million, while layoffs decreased and the number of people quitting increased. “Little changed” doesn’t sound like really exciting news, but in this case, I would argue it is.

I’d expected job openings to cool off, and that would have been fine, since they’re at historically elevated levels. By November (which this report reflects), the impact of the Federal Reserve’s interest rate hikes was being felt throughout the economy, and it was reasonable to anticipate a softening throughout the labor market.

That didn’t happen. A low layoff rate is good news for workers, and a high quit rate indicates they’re still quite confident. And all this happened in November, which was the month with the highest number of tech layoffs in 2022—a good reminder that the tech sector is not the whole economy.

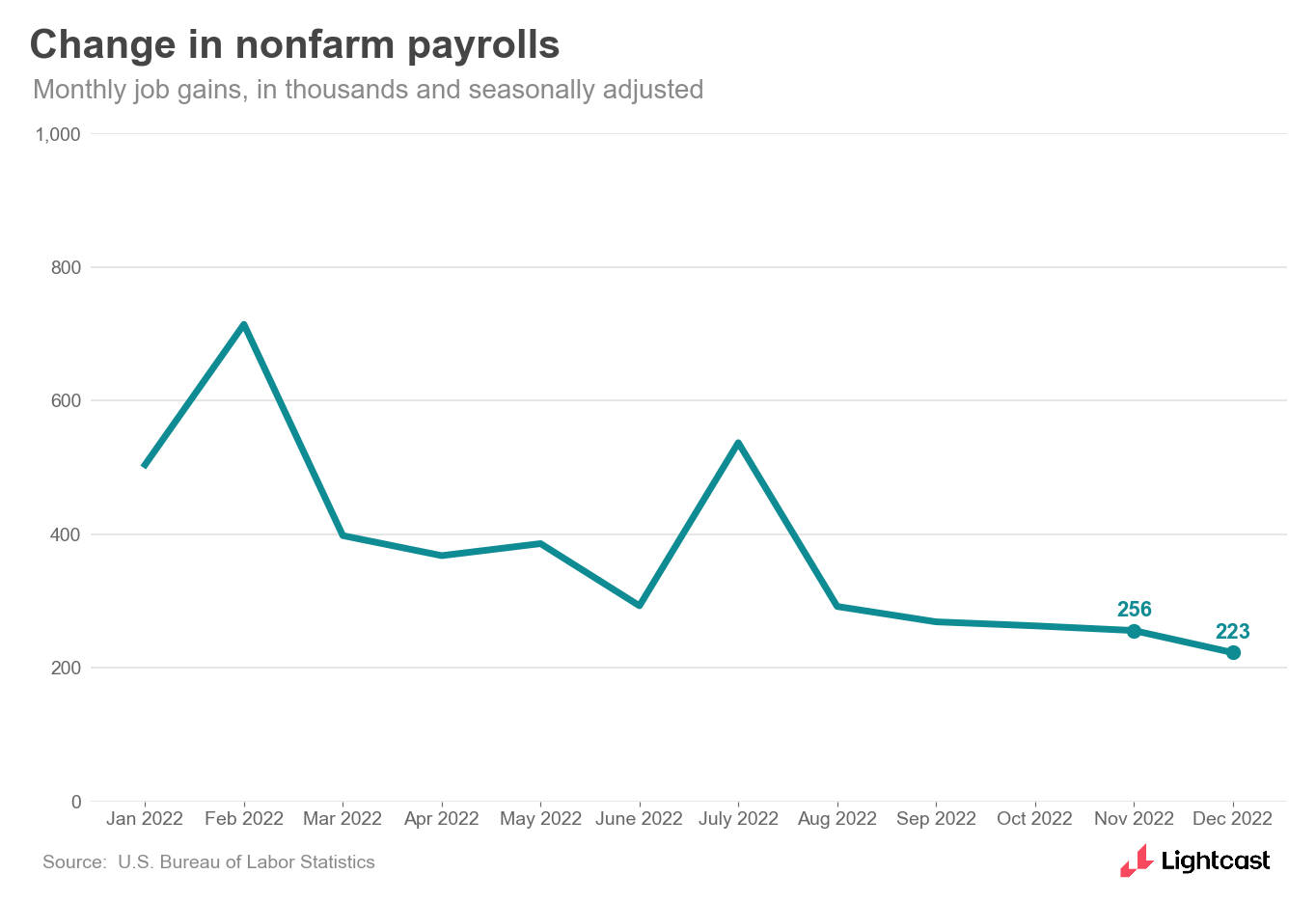

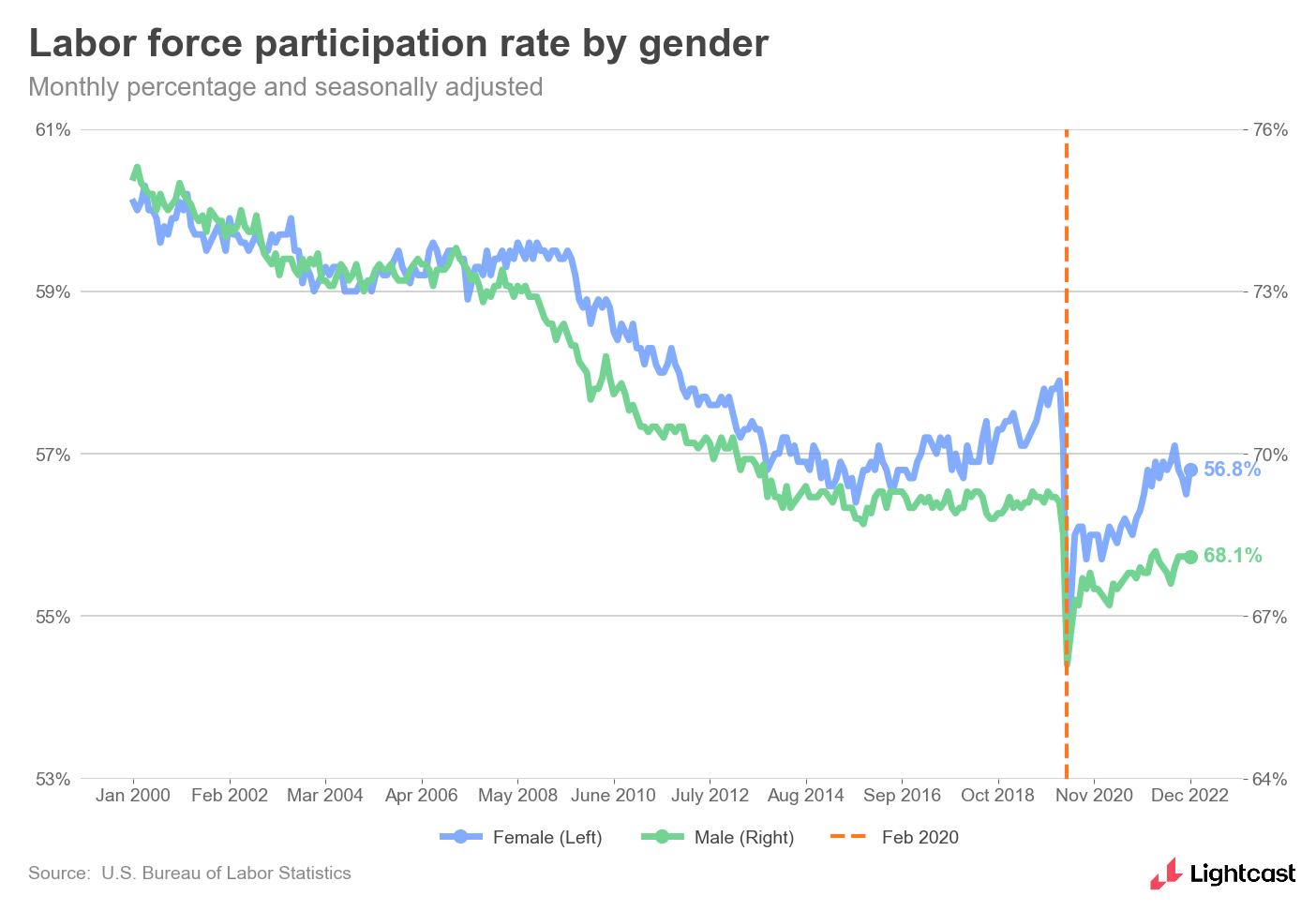

On Friday, the monthly Employment Situation showed similar trends. Employers added 223,000 jobs in December, a decline from the previous month but slightly above expectations, while the unemployment rate fell to 3.5%—tying, once again, its lowest point in decades. We also saw a slight uptick in the labor force participation rate, especially for women.

Overall, this was a surprising set of reports. Usually, the fast pace and large scale of the Fed’s interest rate hikes would have a significant impact on the labor market, even a devastating one. The data clearly shows that isn’t happening so far, and if these trends keep up, we’re going to avoid widespread economic hardship.

That said, you wouldn’t expect many layoffs in November or December—nobody wants to be the villain who puts someone out of a job on Christmas. So if layoffs were in the cards at the end of 2022, they would be borne out in January. (Wall Street has already started us off there).

The January JOLTS, which will be released March 3, will tell us how widespread this pattern is, and it may turn out to be relatively small, affecting only those few organizations. Whatever happens, the reports released last week are better than expected. I was feeling cautious, but now I’m feeling cautiously optimistic—and I wouldn’t anticipate using the word “recession” anytime soon.

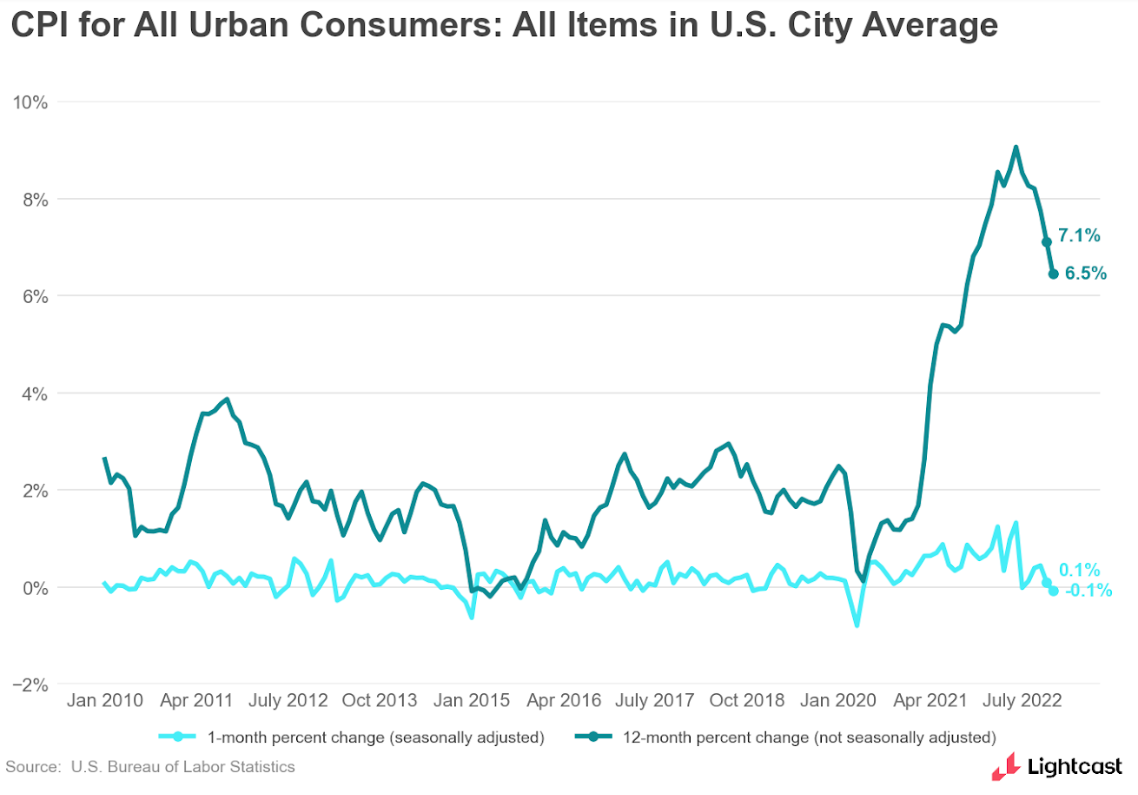

Of course, the Federal Reserve’s role isn’t to cool the labor market, but to tame inflation. A strong labor market is only good news if prices are under control. And today, the CPI gave us a strong signal that they are:

We saw prices go down in December, by 0.1%, bringing the annual level of inflation down to 6.5%. Energy, gas, and used cars saw the biggest decrease—you might even say the used-car market has made a U-turn since the worst of the supply-chain issues sent prices soaring.

This is the first time since the pandemic that we’re seeing prices go down on a monthly basis, and that’s something to feel good about. Unless something drastic and unexpected happens—and in this economy, that’s always a possibility—it looks like we’re going to get inflation under control.

And that raises interesting questions about how the Federal Reserve will react. Up through the end of 2022, they were aggressive in increasing interest rates, but now we’ll want to see how much they moderate. San Francisco Fed President Mary Daly said this week that the bank may increase their interest rate target by 0.25% at its next meeting, down from 0.5% in December. I don’t think the Fed is ready to say its work here is done, but it’s certainly getting closer.

In The Papers

Two papers caught my eye over the break, and I think they speak well to each other. First: “‘The Great Retirement Boom’: The Pandemic-Era Surge in Retirements and Implications for Future Labor Force Participation,” by Joshua Montes, Christopher Smith, and Juliana Dajon showed how the pandemic disrupted the pattern of retirements we were accustomed to seeing through 2019. The retired share of the US population is about 1.5% higher than its pre-pandemic level, and the authors found this accounts “for nearly all of the shortfall in the labor force participation rate.” Pretty significant!

Secondly, “Where Are the Workers? From Great Resignation to Quiet Quitting” by Dain Lee, Jinhyeok Park, and Yongseok Shin found that workers are working dramatically fewer hours over the past three years. The aggregate hours worked per week in the US is down 3%, but only half of that decline is due to fewer people in the labor force. Everyone else is working fewer hours. The decline in hours was greater for men than women, and among men, the decline was greater for those with a bachelor’s degree than those without, and for prime-age workers more than older ones.

We’ve already noted that the US labor force is being stretched thin, but these papers go into important specifics: more people have retired, and those still working are putting in fewer hours. If you have a smaller number of people working for smaller amounts of time, it won’t take long before you feel the effects. And as the news releases showed us, all that change has kept the labor market tight and employees in the driver’s seat.

Until next week,

Bledi Taska

Lightcast Chief Economist