Welcome to the Letter from the Chief Economist.

Keeping Tech Layoffs in Perspective

The top news echoing around the economy these past few weeks has been layoffs at big tech firms, with layoffs numbering in the thousands at Microsoft, Salesforce, Google, Meta, and Amazon. At Lightcast this week, my colleagues and I have shared our perspective on the trend with Barron’s, Axios, and USA Today, among others. Obviously there’s a lot of nuance behind those difficult decisions, but layoffs are bad news for those firms and even more so for the workers feeling the impact.

However, I want to offer what I hope is a reassuring perspective. Two key pieces of context can show us how these layoffs fit into the bigger picture of the entire labor market.

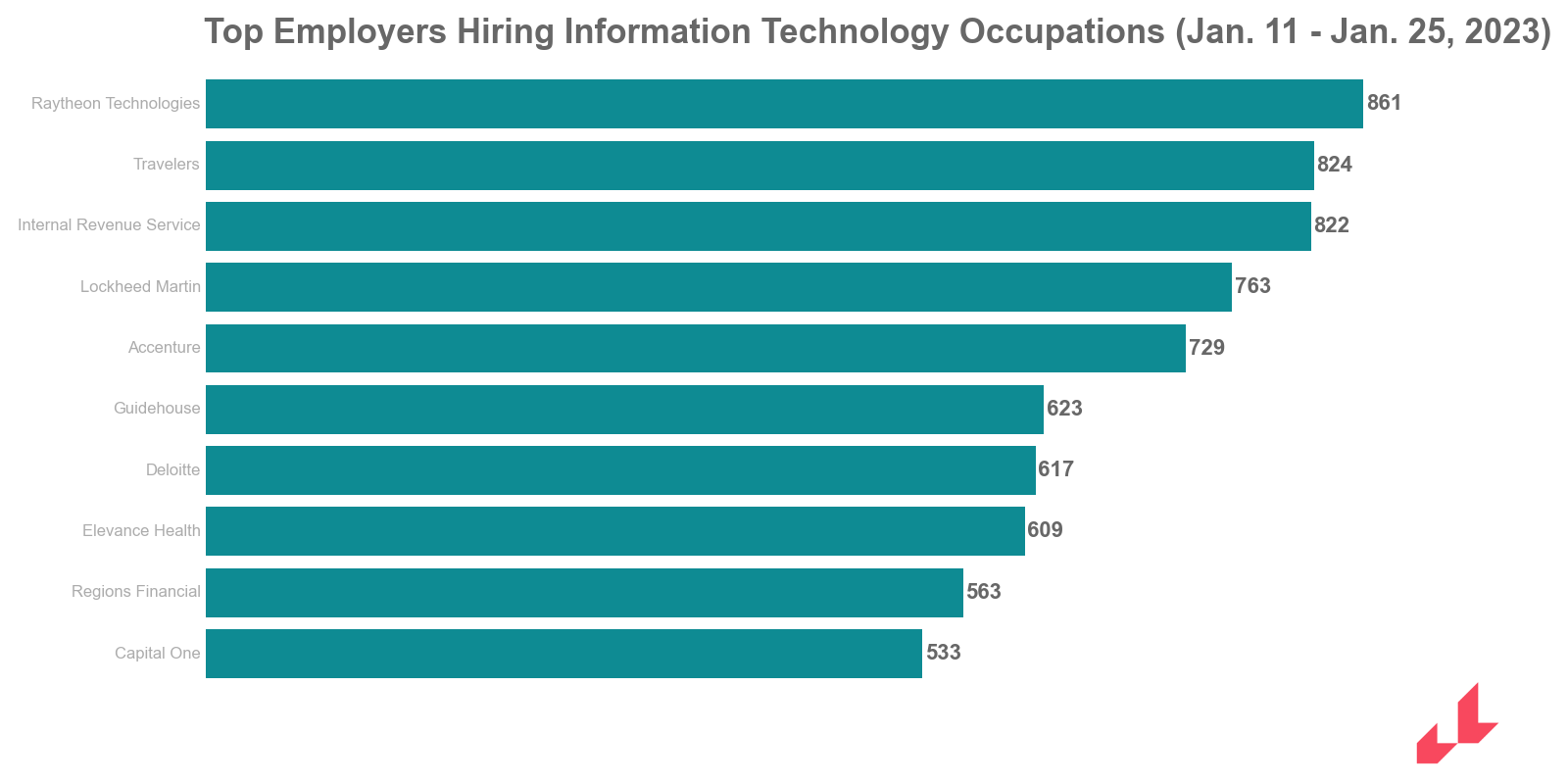

The first is pretty clearly good news: these workers should have little trouble finding new jobs as soon as they want them. The labor market is still historically tight, and their skills are in high demand. In fact, I pulled some Lightcast job posting data to see what demand looks like for workers in IT fields, and several companies have hundreds of openings. These figures are current as of yesterday:

So even if those workers’ old companies aren’t hiring, plenty of others are.

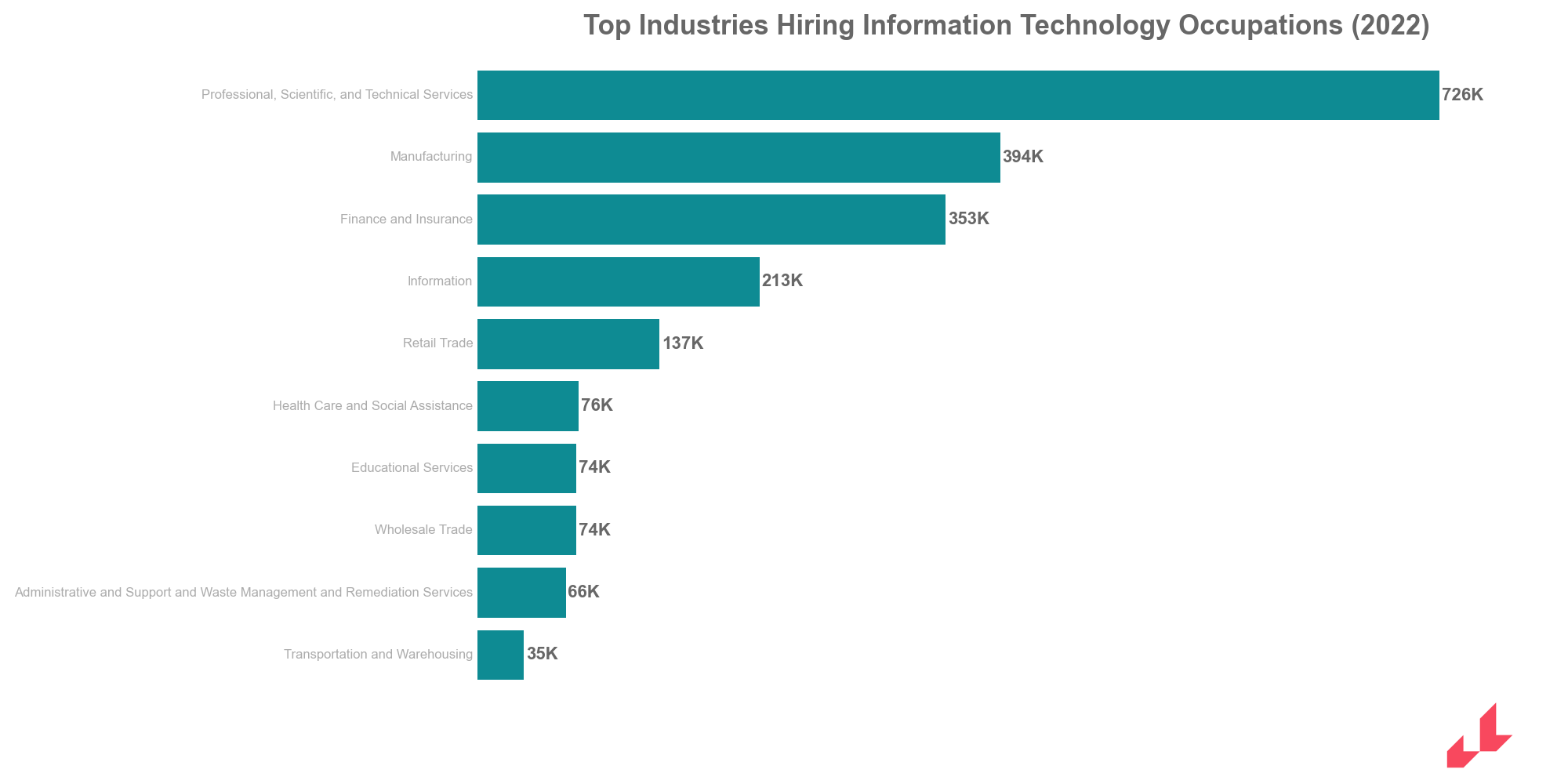

Second, and along a similar line, we need to understand that these big names aren’t the entire economy, and nor are they the entire tech industry. These big names are classified as being part of the “Information” industry by the BLS—but as we can see here, the top industry hiring tech workers (by a large margin) is Professional, Scientific, and Technical Services, followed by Manufacturing and, in third, Finance and Insurance. Information is all the way back in fourth.

We’re all familiar with the big-name tech companies, and almost all of us use their products every day. But one consequence of that familiarity is that we overestimate their impact on the labor market. I would compare it to the relationship between the Ivy League and other schools: they fascinate the public imagination, but there are only eight of them. State universities and community colleges have a much greater impact on American educational life as a whole.

The same holds true for Silicon Valley firms. The big names are big, but tech workers are everywhere, most of them aren’t at these companies, and even fewer were affected by the layoffs.

Before moving away from economic news, I want to note that the BEA’s initial estimate for fourth-quarter GDP came out this morning and it showed 2.9% growth (higher than the 2.6% expected). Over at the Department of Labor, initial jobless claims for this week came in at 186,600, lower than the 205,000 expected. So I’m sorry to everyone who might be hoping for a recession, but it’s not showing up in the numbers.

The Latest from Lightcast

Yesterday saw the release of one of Lightcast’s top annual releases: our 2023 Talent Playbook. The exciting thing about this report is that it’s the first to rely on our global dataset, incorporating international insight from our job postings as we look toward the future of hiring in the coming months. Very briefly, here are the six key takeaways from the report:

Remote work is becoming more common, and employers want people who can work from home and collaborate online. They also want people with specific skills from all over the world.

Jobs related to AI and machine learning are growing, alongside new specific technical skills like working with TikTok and Figma.

Employers are hiring based on skills, and being more transparent about wages.

Wages are growing most for lower-paying jobs, non-white workers and those who have changed jobs.

Companies are now using data to plan for future staffing needs and understand how labor market trends impact hiring and retention costs.

To retain workers that are hard to find, employers are investing in employee development and training, and providing benefits like tuition reimbursement.

It’s a great report, everyone involved in its production and release did an excellent job, and I encourage you to take a look and download the 2023 Global Talent Playbook here.

I also want to take a moment to mention one other update from Lightcast this week: we released a new set of data for CyberSeek, which we created in partnership with CompTIA and the National Initiative for Cybersecurity Education at NIST.

The new data tell us that the demand for cybersecurity was at an all-time high for the first nine months of 2022, despite decreasing in November and December, and over the past three years, private sector cybersecurity demand has grown 36 percent, while public sector demand grew 58 percent. There are 1.1 million workers currently in cybersecurity roles in the US, and over 750,000 openings.

Amid such pressing need, it comes as no surprise that there’s a shortage of workers currently able to meet the need. The supply-demand ratio is currently 68 workers per 100 job openings, indicating the US needs nearly 530,000 more cybersecurity workers in the US in order to close the gap.

To take a closer look at those numbers, and to explore an interactive map and career pathways for cybersecurity workers, be sure to visit the CyberSeek website.

In The Papers

This week’s paper is one of mine—a research brief at the Cato institute alongside my coauthors Gregor Schubert at UCLA and Anna Stansbury at MIT: “Employer Concentration and Outside Options.”

Our focus here is the fact that, in certain geographical areas, there are only a few large employers. We’ve found that high employer concentration is correlated to low pay and stagnant pay growth. Comparing an area with the median level of employer concentration to the 95th percentile, we saw that average wages were 6.5% lower.

This has long been an area of interest for me. In the past, I’ve used Lightcast data to identify the correlation between high concentration and lower wages. Alongside José Azara, Ioana Marinescu, and Marshall Steinbaum, I identified this pattern in “Concentration in US labor markets: Evidence from online vacancy data,” published in Labour Economics—and, I’m proud to add, we won an award for it.

But this research goes further. Instead of just noting the correlation, we wanted to look closer at the actual impact of employer concentration in a market, so we accounted for external trends in our analysis and then measured changes in local employer concentration that were not associated with economic conditions.

When a few employers dominate the labor market, that means less competition for talent, and thus lower wages. According to our estimates, almost one quarter of the workers covered by our data in 2019 experience wage suppression of 2 percent or more as a result of employer concentration. Many of the most affected workers are health care workers, because many parts of the country have a limited number of total medical facilities and often just one hospital.

So where does that leave us? On one hand, there’s a policy angle that could be pursued: antitrust efforts in these high-concentration regions could open up new options for workers there. On a more basic level, what we’ve done here is illuminate a new facet of the labor market—and the better we understand the relationships between workers, skills, employers, and jobs, the better prepared we are to create a job market that works for everyone.

Until next week,

Bledi Taska

Lightcast Chief Economist