Welcome to the Letter from the Chief Economist. After a short break for Thanksgiving, it seems like economic news came back all at once this week. Let’s run through some of the highlights.

JOLTS

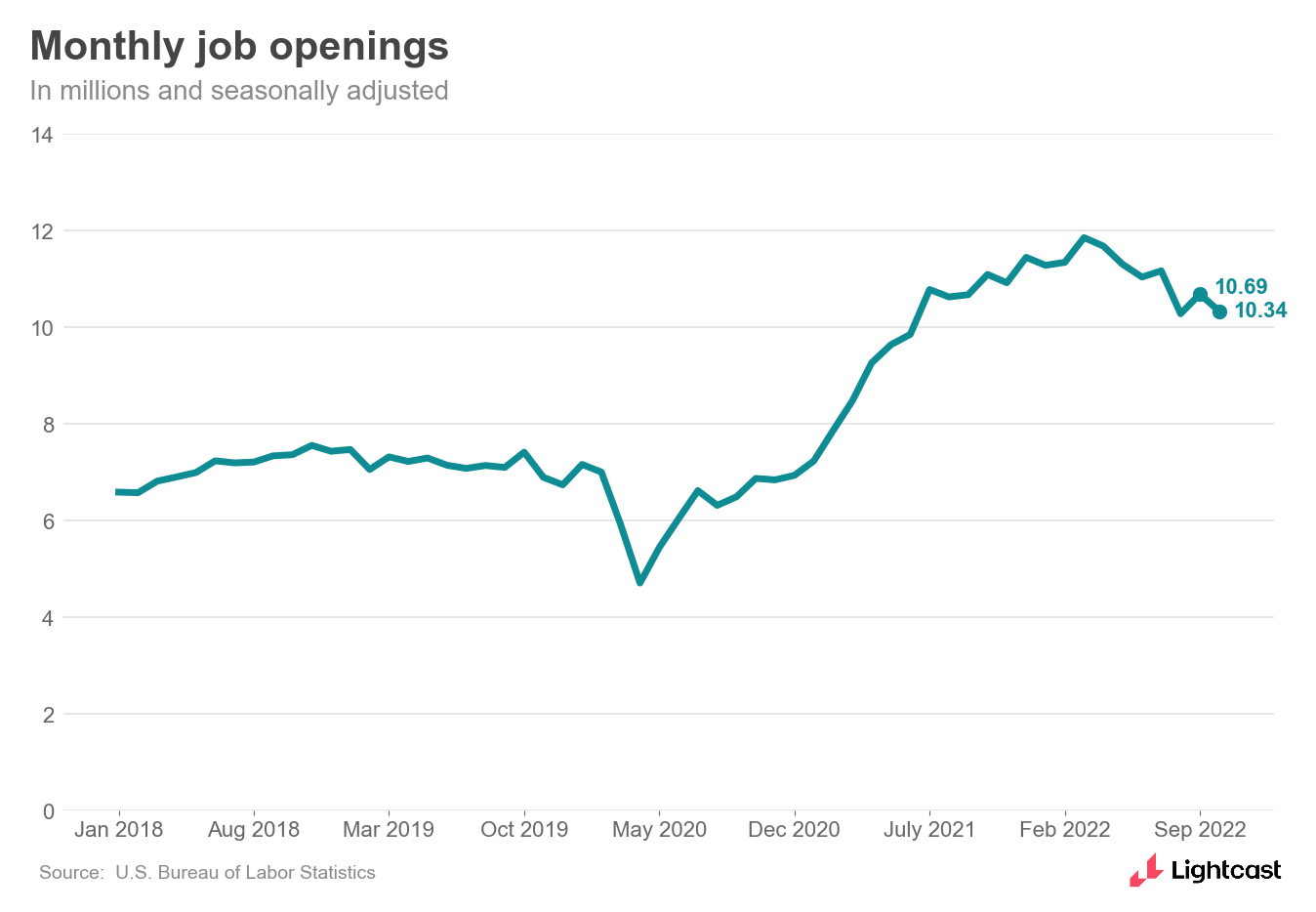

Yesterday’s job openings numbers from the Bureau of Labor Statistics seemed uneventful, but they actually had a lot to tell us.

Job openings declined by 353,000 in October, down to 10.3 million. This brings the number of openings close to where it was in August, after an unexpected jump in September.

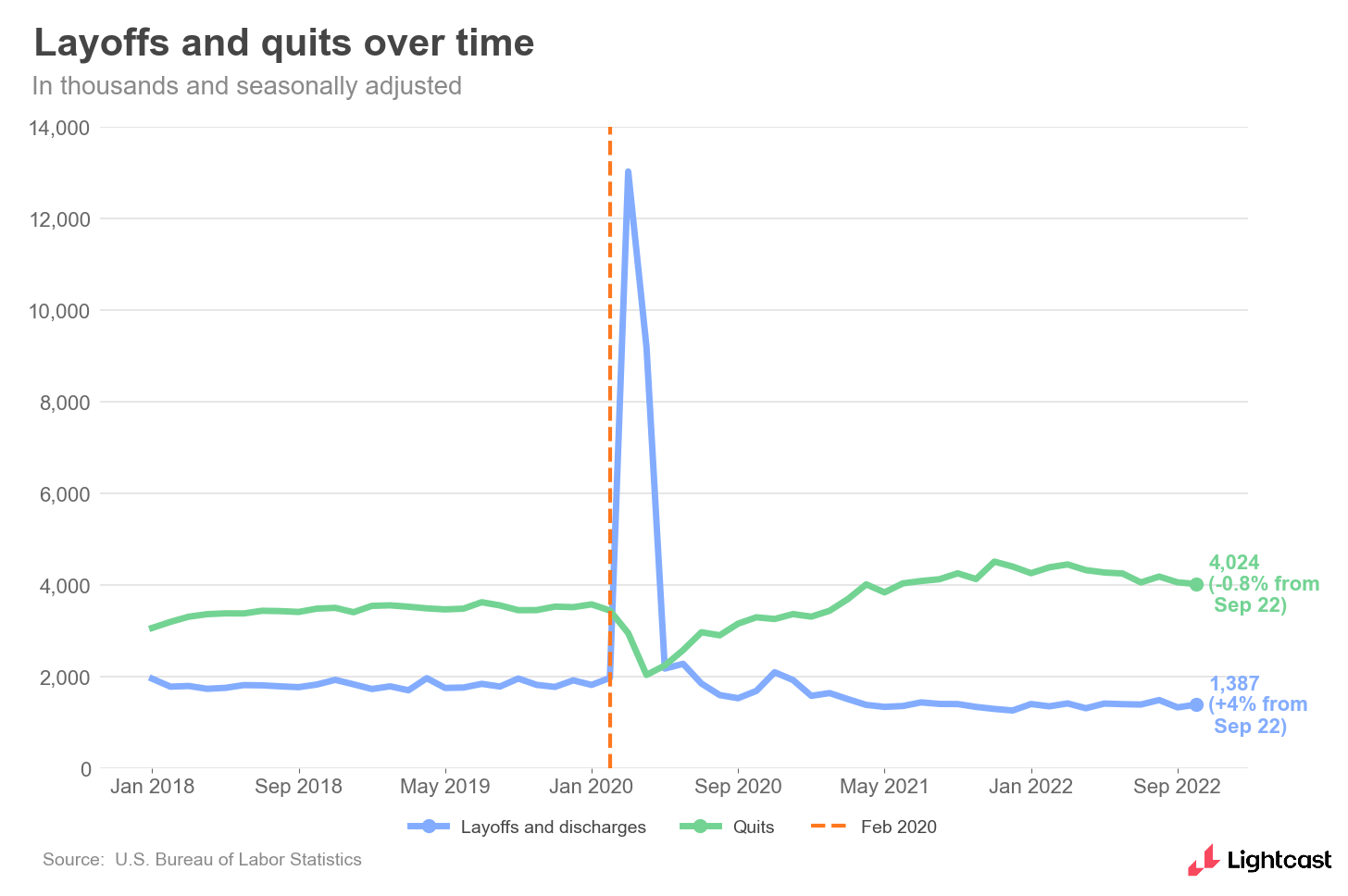

During our live discussion yesterday morning, my colleague Layla O’Kane said her first impression was that “Maybe we will get the soft landing we’ve been hoping for over these past few months,” and I think that’s right. Openings are declining but not plummeting, while quits ticked up and layoffs ticked down—it looks like almost everything in this report changed little, but changed in the right direction.

Thinking back over the past few months, layoffs have been a major topic of discussion, especially at big tech firms. And while this week’s JOLTS showed layoffs are up slightly, it doesn’t seem as though those big-name layoffs are indicating things to come for everyone else. When you hear news about Meta laying off 11,000 people, that should be understood in the context that Meta has also lost $700 billion in value: the layoff says more about the company than it does about the economy.

Is the rest of the economy invulnerable? Of course not. But it’s a much more nuanced picture. Going forward, I would expect much more conservative hiring as opposed to major layoffs.

We’re in a transition phase, and whether we see a recession in the next few months or not, some kind of cooldown is on its way. But I think it’s important to emphasize that after this year’s historically tight labor market, a cooldown isn’t bad news. Even if the market loosens, it won’t be in bad shape.

Of course, the Federal Reserve was looking closely at the JOLTS data to help shape its decisionmaking. And that brings us to another piece of economic news:

Jerome Powell’s Press Conference

The Federal Reserve chair said yesterday that the central bank is likely to maintain a similar approach as it continues to combat inflation, but rate hikes might moderate as soon as its next meeting in two weeks.

I think that makes sense. In fact, I would be very surprised if the Fed doesn’t moderate from an 0.75% interest rate increase down to 0.5%. The bigger question is what happens next.

When the Fed raises rates, its impact is felt slowly, even though the economy and prices are fast-moving and volatile. Inflation shows signs of slowing, and the labor market is less tight than it was this summer, but both are still historically high. If the Fed takes its foot off the brake too early, inflation and the labor market could shoot back up, but interest rates that are too large will discourage investment and cool the economy more than necessary.

So far, so good, but Powell is still in a difficult position. After convening December 13-14, the next Fed policy meeting will be January 31-February 1, so we’ll wait to see how it reacts to the first economic trends of 2023.

Personal Consumption Expenditures

In saying “inflation shows signs of slowing,” the most-quoted measure is the Consumer Price Index, but there are other metrics. The Fed actually prefers the Personal Consumption Expenditures price index, which came out today and showed that prices up are up 6% year-over-year, a decline from the 6.3% yearly increase as of last month’s release.

According to the PCE, spending power ticked town in October. Personal income and disposable personal income rose 0.7% over the month, but expenditures grew just faster, at 0.8%.

The November Employment Situation

When I mentioned we might see more conservative hiring soon, it might be as soon as tomorrow.

Looking forward to the jobs report for November, we’ll want to see a number that’s high enough to show we're not in recession, but low enough that the Fed can ease up on rate hikes. JOLTS did its part; we’ll see if the Employment Situation plays along.

As always, tune in right after the report release to hear our Lightcast senior economists bring their top-tier insight and analysis.

In The Papers

There are two papers I want to touch on this week, both showing how the labor supply is still very low despite the job market loosening up.

The first is on social distancing: restrictions have eased, but its impact hasn’t disappeared completely. “Long Social Distancing” by Jose Maria Barrero, Nicholas Bloom, and Steven J. Davis indicates that over half of all Americans with recent work experience would continue social distancing to some degree even after the end of the pandemic. Their monthly Survey of Working Arrangements and Attitudes found that over 10% of workers would not continue pre-Covid activities like visiting crowded areas or indoor dining, while another 45% would distance in limited ways.

The impact on labor force participation is significant. The researchers’ regression models suggest that “Long Social Distancing” reduced participation by 2.5% in the first half of 2022, and the ongoing impact will persist for the foreseeable future. The NBER Digest provides a good overview of the paper with a little more detail.

The second paper—“International College Students' Impact on the US Skilled Labor Supply,” by Michel Beine, Giovanni Peri, and Morgan Raux—shows the impact of foreign-born US college students on the local workforce where they went to school. They found that nearly a quarter of all foreign-born graduates with a master’s degree (and 11% of those with a bachelor’s degree) stayed in their institution’s state for their first job after graduation. The percentages are even higher for graduates with STEM degrees.

This matters for the labor force because it provides a reliable estimate to help shape education and immigration policy. By admitting 100,000 new master’s degree students into the country, the US could expect to add 23,000 new (and highly-skilled) workers to a labor force that still badly needs them. There’s also a good summary of this paper in the NBER Digest with the actual statistics on international enrollment.

As always, more data continues to give us a better view of an unpredictable labor market. It’s been a busy few weeks, and with the Employment Situation tomorrow, we’re not done yet.

Until next week,

Bledi Taska

Lightcast Chief Economist