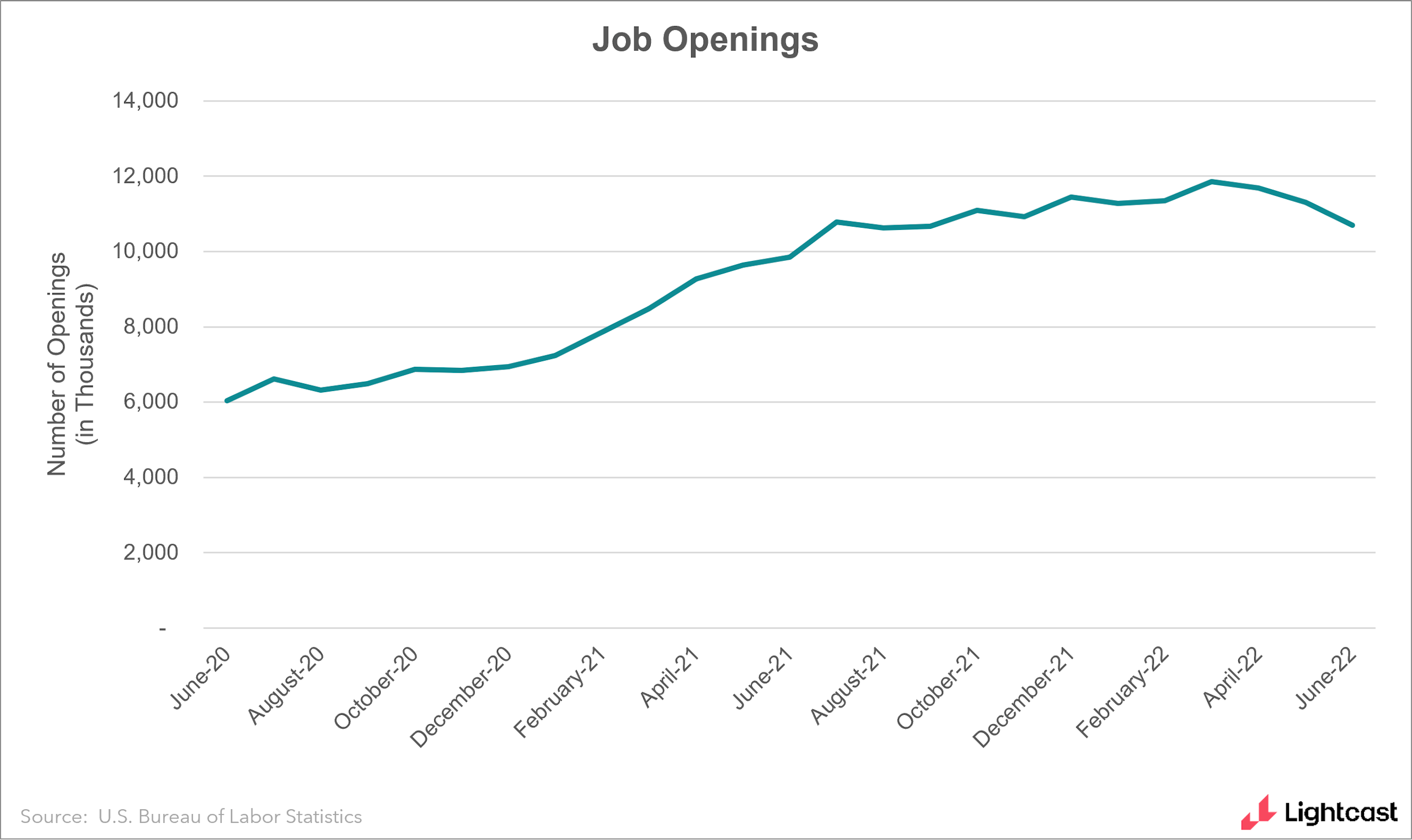

It’s a big week for economic news, after an unexpected JOLTS on Tuesday and a highly-anticipated Employment Situation on Friday. The BLS reported there were 10.7 million US job openings in June, down from 11.3 million in May and lower than the 11 million economists predicted.

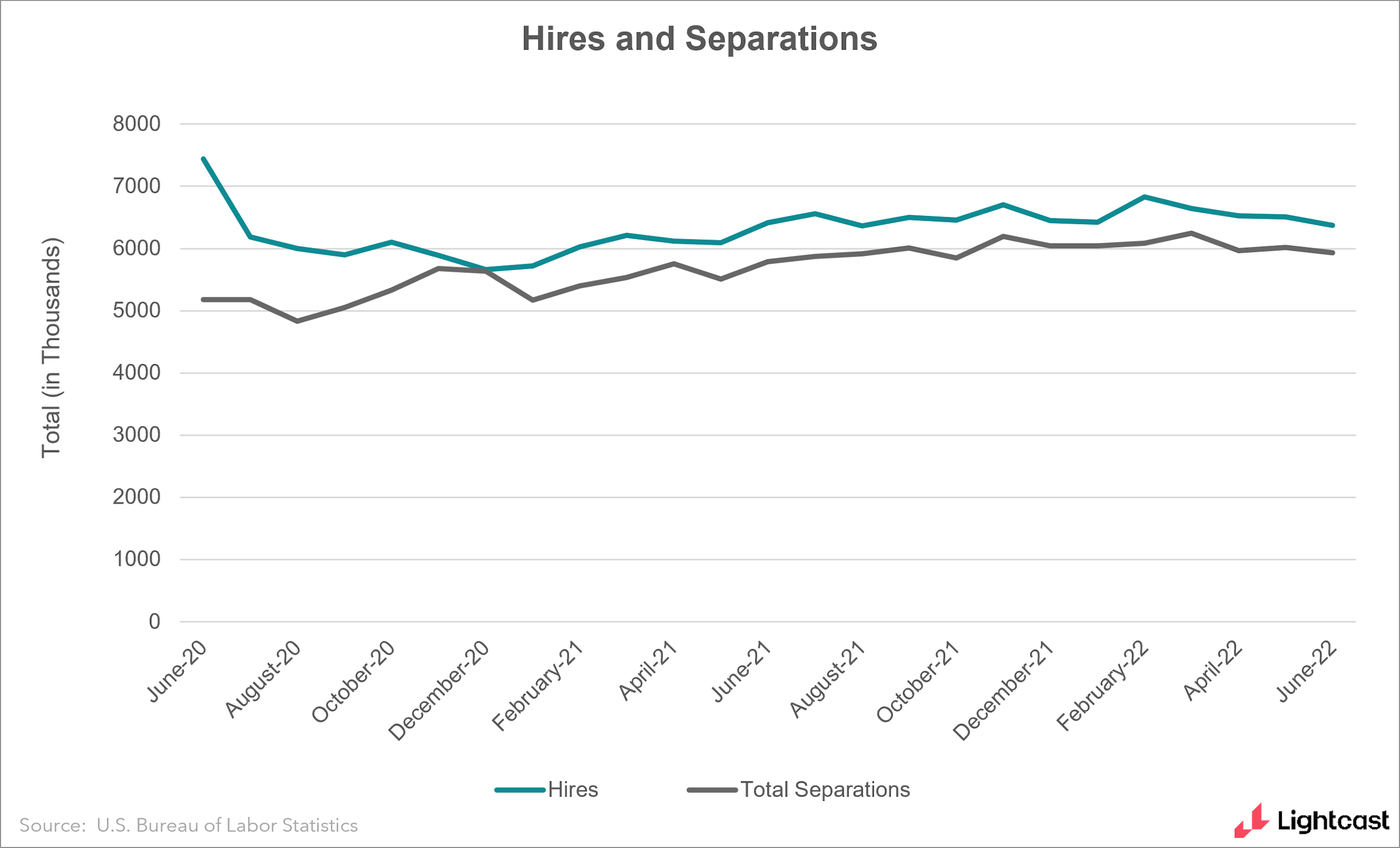

But despite the bigger-than-anticipated drop, I was struck by how strong the labor market still looked. Quits dipped a little (from 4.33 million to 4.27 million), but that’s still historically high, and that tells me that worker confidence is still high as well. People feel empowered to go out and find better jobs with better pay, more flexibility, or whatever combination of factors matters most to them. And often, it’s working: according to new analysis from the Pew Research Center, 60% of workers who changed jobs in the twelve months ending March 2022 saw a real wage increase, compared to 47% of those who stay at their jobs.

While quits stayed high, layoffs remained low. In fact, JOLTS told us the layoff rate actually decreased slightly in June, the opposite of what we’ve seen in the media about downsizing at high-profile firms (the latest victims being Robinhood and Oracle). Processional and Business Services, the category including tech jobs in JOLTS, saw a decrease in layoffs as well. While it’s true that scattered tech layoffs are happening, the data show us that the rest of the economy hasn’t been feeling the same pressure—not in June, at least.

This brings me to the bigger questions about a recession, the Federal Reserve, and how this data fits into the bigger economic puzzle. After we saw that GDP showed negative growth for the second straight quarter (as I mentioned in last week’s newsletter), we’ve been looking for signs that we’re in a recession.

But why are we worried about a recession? In the past, such as in 2008, recessions have meant people lose work or even their houses, facing real hardship because of where the economy as a whole was going. That’s not happening this time. Job openings are down, but looking across the labor market, very few people are losing the jobs they already have. That’s good news.

It’s good news for the Federal Reserve especially as it tries to engineer a “soft landing” as the labor market and inflation both come down from historic highs. Worker earnings are rising more slowly than inflation, mitigating concerns about a wage-price spiral, and the drop in job openings is bringing the labor market closer to a historical normal after its unprecedented tightness earlier this year. That looks like a soft landing to me.

After the report on Tuesday, I shared many of these thoughts, as well as other first impressions with my colleagues Layla O’Kane and Christopher Laney, and you can watch that discussion on the Lightcast LinkedIn page. When the July Employment Situation report comes out Friday, catch Lightcast Senior Economists Rucha Vankudre and Ron Hetrick on their own broadcast. In addition to the jobs number, I’ll also be watching closely to see if earnings have risen more in the face of inflation.

In The Papers

After working in data as long as I have, there’s one problem that I’ve run into time and time again: how do you value the “data economy” —the huge boost in productivity brought about by big data? But now we’ve found a solution.

“Valuing the US Data Economy Using Machine Learning and Online Job Postings,” by José Bayoán Santiago Calderón and Dylan G. Rassier at the Bureau of Economic Analysis shows how they’ve developed a way of using machine learning to provide a reliable estimate of data-related skills and their economic value.

What Calderón and Rassier did is look at information from Lightcast job postings as a way to measure the value of data-related work (using data-intensive occupations like statisticians as benchmarks), and find the value of the data itself from there. In applying that method to a conservative definition of the data economy (to align with GDP standards), they estimated annual investment in data-relevant activities grew about 4.4% annually from 2010–2019, going from $88.3 billion to $130.8 billion in current dollars.

This type of measurement has been a high priority for all kinds of statistical agencies, and I’m looking forward to seeing it applied to more challenging problems, like valuing data and software in GDP (as discussed by researchers at OECD earlier this year and the NBER in 2019).

At Lightcast, the importance and value of good data is always at the front of our minds, and finding new and innovative ways of applying it presents new possibilities about the knowledge and solutions we can unlock for our clients and in our own research. It’s exciting to see.

Until next week,

Bledi Taska

Lightcast Chief Economist