What goes up must come down. Or at least that’s what usually happens.

But when it comes to the labor market, it’s harder to say for sure. This week, we had two big pieces of economic news that highlighted how the labor market refuses to slow down—and how much that matters to the rest of the economy.

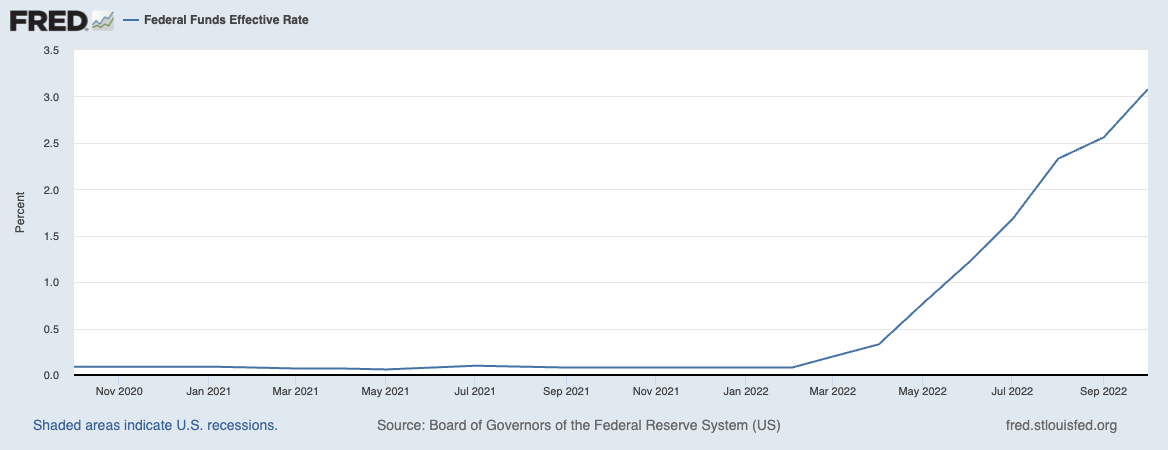

The biggest piece of news came from the Federal Reserve’s Federal Open Market Committee, which met yesterday and raised interest rates by 0.75% for the fifth straight meeting, a widely-anticipated move that many still see as cause for concern, especially outside the US, because the ongoing increases may risk a global economic downturn.

I took this graph from FRED to show just how steep the interest-rate increase has been over the past two years.

Fed Chairman Jerome Powell acknowledged during his remarks yesterday that ongoing inflation “narrows the path to a soft landing,” where price increases cool without triggering widespread economic hardship.

He also signaled that interest-rate hikes might taper off in the future into smaller, longer-term increases, rather than the sharp spike we’ve seen recently. The Fed does seem determined, though, that inflation won’t cool until the labor market does, and Powell doesn’t see that happening.

“Maybe that’s there, but it’s not obvious to me,” he said. “The labor market is just very, very strong, and households, of course, have strong balance sheets...it will take some time for inflation to come down.”

So what evidence was Powell looking for to see whether the labor market had cooled? I’m glad you asked.

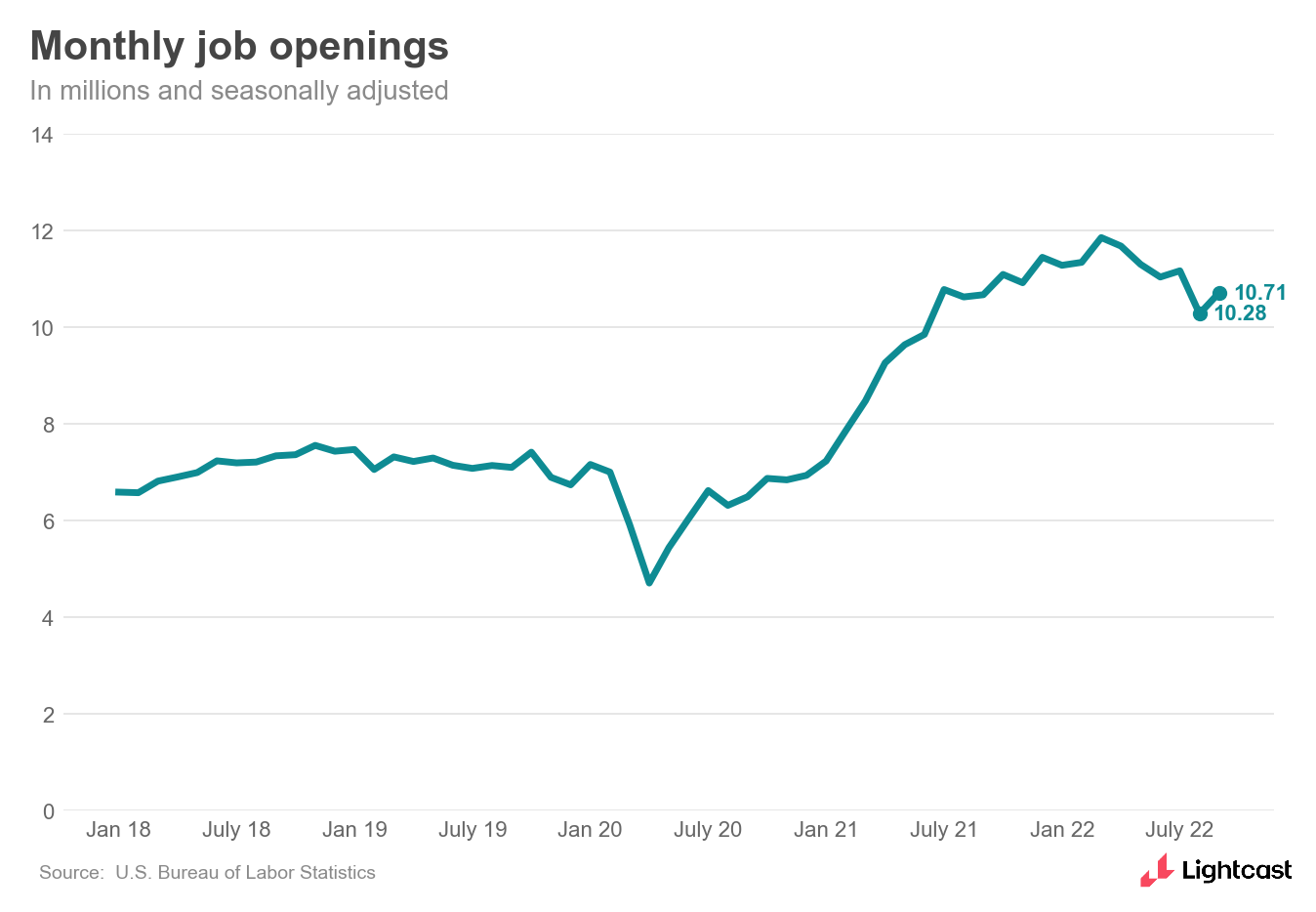

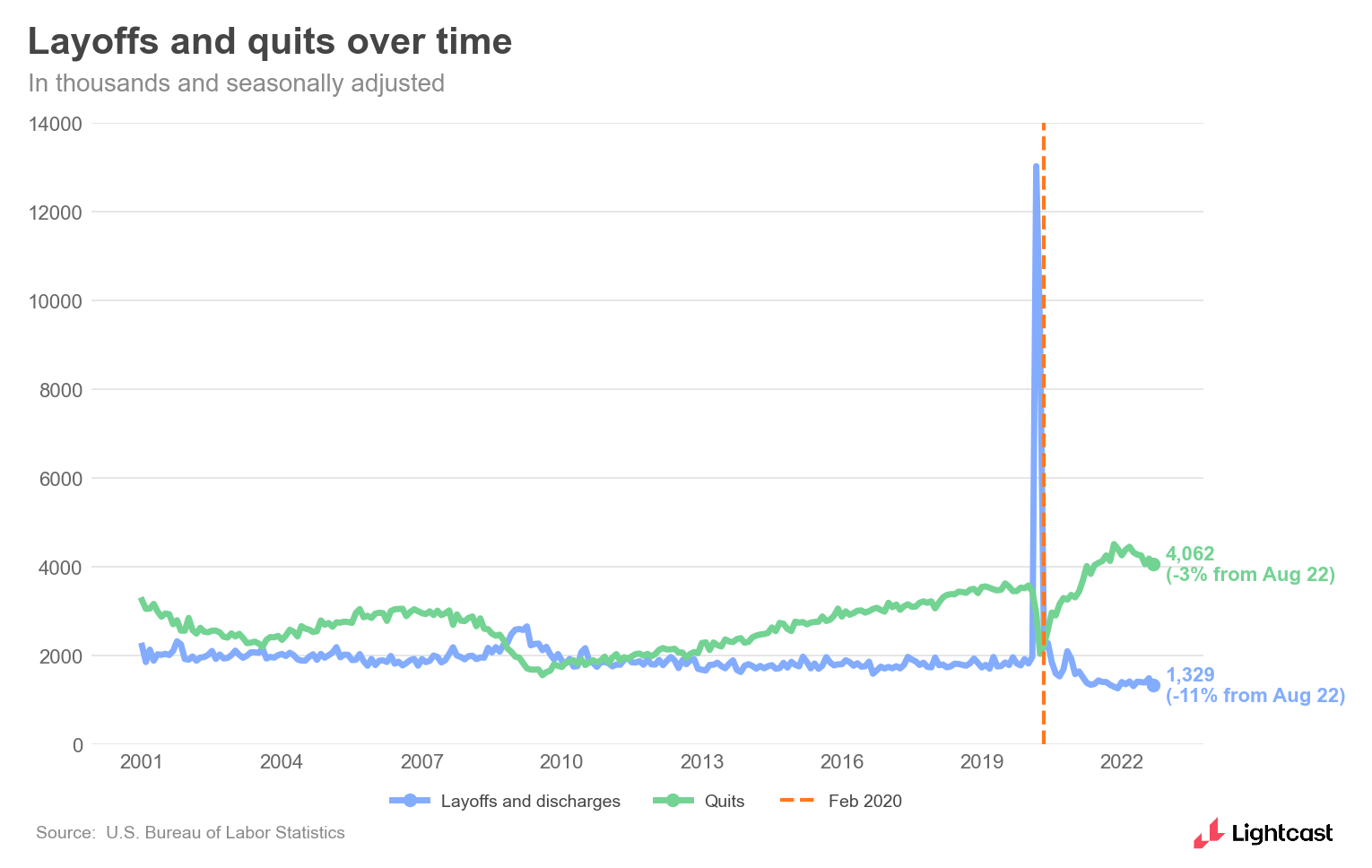

The Fed’s meeting was on Wednesday; on Tuesday, we had JOLTS. Job openings were widely predicted to continue declining from their record highs (what goes up must come down), but instead, job openings went back up in September, moving from 10.3 million to 10.7 million. Quits held steady and layoffs declined slightly, showing that workers are still confident about finding new jobs and businesses are still reluctant to give up their existing workforce.

Every indicator shows that the labor market is showing remarkable resilience. I went into more detail about this Tuesday morning with my colleague Layla O’Kane during a live discussion about the report, which you can revisit here. Tomorrow morning, Lightcast Senior Economists Ron Hetrick and Rucha Vankudre will host their own discussion on the monthly Employment Situation report, so be sure to join them for that at 9:00 a.m. ET/6:00 PT tomorrow. (And on that note, I’d also expect job gains to cool some but remain historically elevated when we see the new data tomorrow.)

Overall, this is a very healthy economy. Consumer savings are high, and this sets us up for a strong holiday shopping season, especially because workers don’t feel like their job is on the line, therefore they don’t need to be overly cautious about their spending.

That’s good news for everyone…except Jerome Powell.

In The Papers

We’ve always paid special attention to artificial intelligence (AI) here at Lightcast; eagle-eyed readers will remember a few weeks ago I shared this paper I helped write, where my co-authors and I found evidence that machine learning is on its way to becoming a “general purpose technology” on the world-changing scale of electricity or the internet. As a company, we’ve also worked with the Artificial Intelligence Lab at Stanford and published AI research internationally, as well.

This week, I’m looking at two papers that study AI’s contribution to productivity and worker success: “Automation After the Assembly Line” by Leah Platt Boustan, Jiwon Choi, and David Clingingsmith; and “AI, Skill, and Productivity: The Case of Taxi Drivers,” by Kyogo Kanazawa, Daiji Kawaguchi, Hitoshi Shigeoka, and Yasutora Watanabe.

The first paper goes into detail about the prevalence of AI and robotics tools in factories and includes a novel measure on exposure to those tools. In other words, they were able to sort workers by how much they worked with automated manufacturing, then studied their outcomes. The paper found that higher exposure to computerized machines was correlated with higher productivity, higher educational attainment (as relevant degree programs also expanded), and total employment rose, with the highest gains in unionized jobs.

The second feels almost like science-fiction: the authors studied an AI tool that helped taxi drivers by predicting routes where demand was expected to be high. The AI improved driver productivity and shortened cruising time—but interestingly, that gain was overwhelmingly concentrated among drivers that were less experienced. The productivity gap between high-skill and low-skill drivers narrowed by 14%.

The taxi-driver data shows that AI has more to teach us than a simple story about job displacement, and that it can also help reveal and guide insights about worker productivity and create more equity in the workforce. The manufacturing data was also very encouraging, as it shows that a workforce benefits across the board when augmented with AI, which is a promising sign as we continue to navigating the complex labor market—no matter if what goes up ever comes down or not.

Until next week,

Bledi Taska

Lightcast Chief Economist